Forecasting Time Series - In Depth#

![]()

This tutorial provides an in-depth overview of the time series forecasting capabilities in AutoGluon. Specifically, we will cover:

What is probabilistic time series forecasting?

Forecasting time series with additional information

What data format is expected by

TimeSeriesPredictor?How to evaluate forecast accuracy?

Which forecasting models are available in AutoGluon?

What functionality does

TimeSeriesPredictoroffer?Basic configuration with

presetsandtime_limitManually selecting what models to train

Hyperparameter tuning

This tutorial assumes that you are familiar with the contents of Forecasting Time Series - Quick Start.

What is probabilistic time series forecasting?#

A time series is a sequence of measurements made at regular intervals.

The main objective of time series forecasting is to predict the future values of a time series given the past observations.

A typical example of this task is demand forecasting.

For example, we can represent the number of daily purchases of a certain product as a time series.

The goal in this case could be predicting the demand for each of the next 14 days (i.e., the forecast horizon) given the historical purchase data.

In AutoGluon, the prediction_length argument of the TimeSeriesPredictor determines the length of the forecast horizon.

The objective of forecasting could be to predict future values of a given time series, as well as establishing prediction intervals within which the future values will likely lie.

In AutoGluon, the TimeSeriesPredictor generates two types of forecasts:

mean forecast represents the expected value of the time series at each time step in the forecast horizon.

quantile forecast represents the quantiles of the forecast distribution. For example, if the

0.1quantile (also known as P10, or the 10th percentile) is equal tox, it means that the time series value is predicted to be belowx10% of the time. As another example, the0.5quantile (P50) corresponds to the median forecast. Quantiles can be used to reason about the range of possible outcomes. For instance, by the definition of the quantiles, the time series is predicted to be between the P10 and P90 values with 80% probability.

By default, the TimeSeriesPredictor outputs the quantiles [0.1, 0.2, 0.3, 0.4, 0.5, 0.6, 0.7, 0.8, 0.9]. Custom quantiles can be provided with the quantile_levels argument

predictor = TimeSeriesPredictor(quantile_levels=[0.05, 0.5, 0.95])

Forecasting time series with additional information#

In real-world forecasting problems we often have access to additional information, beyond just the raw time series values. AutoGluon supports two types of such additional information: static features and time-varying covariates.

Static features#

Static features are the time-independent attributes (metadata) of a time series. These may include information such as:

location, where the time series was recorded (country, state, city)

fixed properties of a product (brand name, color, size, weight)

store ID or product ID

Providing this information may, for instance, help forecasting models generate similar demand forecasts for stores located in the same city.

In AutoGluon, static features are stored as an attribute of a TimeSeriesDataFrame object.

As an example, let’s have a look at the M4 Daily dataset.

import pandas as pd

from autogluon.timeseries import TimeSeriesDataFrame, TimeSeriesPredictor

We download a subset of 100 time series as a TimeSeriesDataFrame

train_data = TimeSeriesDataFrame.from_path(

"https://autogluon.s3.amazonaws.com/datasets/timeseries/m4_daily_subset/train.csv",

)

train_data.head()

| target | ||

|---|---|---|

| item_id | timestamp | |

| D1737 | 1995-05-23 12:00:00 | 1900.0 |

| 1995-05-24 12:00:00 | 1877.0 | |

| 1995-05-25 12:00:00 | 1873.0 | |

| 1995-05-26 12:00:00 | 1859.0 | |

| 1995-05-27 12:00:00 | 1876.0 |

AutoGluon expects static features as a pandas.DataFrame object, where the index column includes all the item_ids present in the respective TimeSeriesDataFrame.

static_features = pd.read_csv(

"https://autogluon.s3.amazonaws.com/datasets/timeseries/m4_daily_subset/metadata.csv",

index_col="item_id",

)

static_features.head()

| domain | |

|---|---|

| item_id | |

| D1737 | Industry |

| D1843 | Industry |

| D2246 | Finance |

| D909 | Micro |

| D1345 | Micro |

In the M4 Daily dataset, there is a single categorical static feature that denotes the domain of origin for each time series.

We attach the static features to a TimeSeriesDataFrame as follows

train_data.static_features = static_features

If static_features doesn’t contain some item_ids that are present in train_data, an exception will be raised.

Now, when we fit the predictor, all models that support static features will automatically use the static features included in train_data.

predictor = TimeSeriesPredictor(prediction_length=14).fit(train_data)

...

Following types of static features have been inferred:

categorical: ['domain']

continuous (float): []

...

This message confirms that column 'domain' was interpreted as a categorical feature.

In general, AutoGluon-TimeSeries supports two types of static features:

categorical: columns of dtypeobject,stringandcategoryare interpreted as discrete categoriescontinuous: columns of dtypeintandfloatare interpreted as continuous (real-valued) numberscolumns with other dtypes are ignored

To override this logic, we need to manually change the columns dtype.

For example, suppose the static features data frame contained an integer-valued column "store_id".

train_data.static_features["store_id"] = list(range(len(train_data.item_ids)))

By default, this column will be interpreted as a continuous number.

We can force AutoGluon to interpret it a a categorical feature by changing the dtype to category.

train_data.static_features["store_id"] = train_data.static_features["store_id"].astype("category")

Note: If training data contained static features, the predictor will expect that data passed to predictor.predict(), predictor.leaderboard(), and predictor.evaluate() also includes static features with the same column names and data types.

Time-varying covariates#

Covariates are the time-varying features that may influence the target time series. They are sometimes also referred to as dynamic features, exogenous regressors, or related time series. AutoGluon supports two types of covariates:

known covariates that are known for the entire forecast horizon, such as

holidays

day of the week, month, year

promotions

past covariates that are only known up to the start of the forecast horizon, such as

sales of other products

temperature, precipitation

transformed target time series

In AutoGluon, both known_covariates and past_covariates are stored as additional columns in the TimeSeriesDataFrame.

We will again use the M4 Daily dataset as an example and generate both types of covariates:

a

past_covariateequal to the logarithm of the target time series:a

known_covariatethat equals to 1 if a given day is a weekend, and 0 otherwise.

import numpy as np

train_data["log_target"] = np.log(train_data["target"])

WEEKEND_INDICES = [5, 6]

timestamps = train_data.index.get_level_values("timestamp")

train_data["weekend"] = timestamps.weekday.isin(WEEKEND_INDICES).astype(float)

train_data.head()

| target | log_target | weekend | ||

|---|---|---|---|---|

| item_id | timestamp | |||

| D1737 | 1995-05-23 12:00:00 | 1900.0 | 7.549609 | 0.0 |

| 1995-05-24 12:00:00 | 1877.0 | 7.537430 | 0.0 | |

| 1995-05-25 12:00:00 | 1873.0 | 7.535297 | 0.0 | |

| 1995-05-26 12:00:00 | 1859.0 | 7.527794 | 0.0 | |

| 1995-05-27 12:00:00 | 1876.0 | 7.536897 | 1.0 |

When creating the TimeSeriesPredictor, we specify that the column "target" is our prediction target, and the

column "weekend" contains a covariate that will be known at prediction time.

predictor = TimeSeriesPredictor(

prediction_length=14,

target="target",

known_covariates_names=["weekend"],

).fit(train_data)

Predictor will automatically interpret the remaining columns (except target and known covariates) as past covariates. This information is logged during fitting:

...

Provided dataset contains following columns:

target: 'target'

known covariates: ['weekend']

past covariates: ['log_target']

...

Finally, to make predictions, we generate the known covariates for the forecast horizon

from autogluon.timeseries.utils.forecast import get_forecast_horizon_index_ts_dataframe

future_index = get_forecast_horizon_index_ts_dataframe(train_data, prediction_length=14)

future_timestamps = future_index.get_level_values("timestamp")

known_covariates = pd.DataFrame(index=future_index)

known_covariates["weekend"] = future_timestamps.weekday.isin(WEEKEND_INDICES).astype(float)

known_covariates.head()

| weekend | ||

|---|---|---|

| item_id | timestamp | |

| D1737 | 1997-05-28 12:00:00 | 0.0 |

| 1997-05-29 12:00:00 | 0.0 | |

| 1997-05-30 12:00:00 | 0.0 | |

| 1997-05-31 12:00:00 | 1.0 | |

| 1997-06-01 12:00:00 | 1.0 |

Note that known_covariates must satisfy the following conditions:

The columns must include all columns listed in

predictor.known_covariates_namesThe

item_idindex must include all item ids present intrain_dataThe

timestampindex must include the values forprediction_lengthmany time steps into the future from the end of each time series intrain_data

If known_covariates contain more information than necessary (e.g., contain additional columns, item_ids, or timestamps),

AutoGluon will automatically select the necessary rows and columns.

Finally, we pass the known_covariates to the predict function to generate predictions

predictor.predict(train_data, known_covariates=known_covariates)

The list of models that support static features and covariates is available in Forecasting Model Zoo.

What data format is expected by TimeSeriesPredictor?#

There are several assumptions that AutoGluon places on the data to ensure that all models can work as expected:

All time series must have length ≥ 3.

Training data must contain at least some time series with length ≥

2 * prediction_length + 1. This is necessary to ensure that there is some data available to use as an internal validation set.All time series must be regularly sampled (e.g., measurements made every day).

There are no missing values in the data.

Note that all time series in the dataset can have different lengths.

Handling irregular data and missing values#

In some applications, like finance, data often comes with irregular measurements (e.g., no stock price is available for weekends or holidays) or missing values. AutoGluon provides utilities for fixing such problems with the data.

Here is an example of a dataset with an irregular time index:

df_irregular = TimeSeriesDataFrame(

pd.DataFrame(

{

"item_id": [0, 0, 0, 1, 1],

"timestamp": ["2022-01-01", "2022-01-02", "2022-01-04", "2022-01-01", "2022-01-04"],

"target": [1, 2, 3, 4, 5],

}

)

)

df_irregular

| target | ||

|---|---|---|

| item_id | timestamp | |

| 0 | 2022-01-01 | 1 |

| 2022-01-02 | 2 | |

| 2022-01-04 | 3 | |

| 1 | 2022-01-01 | 4 |

| 2022-01-04 | 5 |

We can fill the gaps in the time index using the method TimeSeriesDataFrame.to_regular_index().

Here we specify freq="D" to indicate that the filled index must have a daily frequency

(see other possible choices in pandas documentation).

df_regular = df_irregular.to_regular_index(freq="D")

df_regular

| target | ||

|---|---|---|

| item_id | timestamp | |

| 0 | 2022-01-01 | 1.0 |

| 2022-01-02 | 2.0 | |

| 2022-01-03 | NaN | |

| 2022-01-04 | 3.0 | |

| 1 | 2022-01-01 | 4.0 |

| 2022-01-02 | NaN | |

| 2022-01-03 | NaN | |

| 2022-01-04 | 5.0 |

We can verify that the index is now regular and has a daily frequency

print(f"Data has frequency '{df_regular.freq}'")

Data has frequency 'D'

However, now the data contains missing values represented by NaN.

To fill the NaNs, we use the method TimeSeriesDataFrame.fill_missing_values() that implements various imputation strategies.

df_filled = df_regular.fill_missing_values()

df_filled

| target | ||

|---|---|---|

| item_id | timestamp | |

| 0 | 2022-01-01 | 1.0 |

| 2022-01-02 | 2.0 | |

| 2022-01-03 | 2.0 | |

| 2022-01-04 | 3.0 | |

| 1 | 2022-01-01 | 4.0 |

| 2022-01-02 | 4.0 | |

| 2022-01-03 | 4.0 | |

| 2022-01-04 | 5.0 |

Now the data has a regular index and contains no missing values, so it can be used to train a TimeSeriesPredictor.

How to evaluate forecast accuracy?#

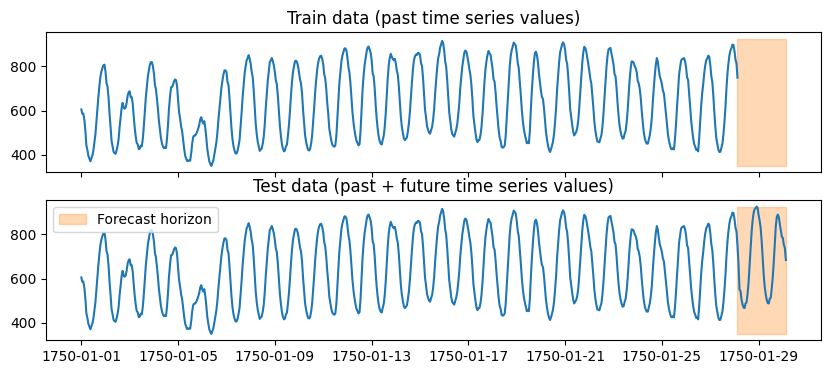

To measure how accurately TimeSeriesPredictor can forecast unseen time series, we need to reserve some test data that won’t be used for training.

This can be easily done using the train_test_split method of a TimeSeriesDataFrame:

prediction_length = 48

data = TimeSeriesDataFrame.from_path("https://autogluon.s3.amazonaws.com/datasets/timeseries/m4_hourly_subset/train.csv")

train_data, test_data = data.train_test_split(prediction_length)

We obtained two TimeSeriesDataFrames from our original data:

test_datacontains exactly the same data as the originaldataIn

train_data, the lastprediction_lengthtime steps are removed from the end of each time series

import matplotlib.pyplot as plt

import numpy as np

item_id = "H1"

fig, (ax1, ax2) = plt.subplots(nrows=2, figsize=[10, 4], sharex=True)

train_ts = train_data.loc[item_id]

test_ts = test_data.loc[item_id]

ax1.set_title("Train data (past time series values)")

ax1.plot(train_ts)

ax2.set_title("Test data (past + future time series values)")

ax2.plot(test_ts)

for ax in (ax1, ax2):

ax.fill_between(np.array([train_ts.index[-1], test_ts.index[-1]]), test_ts.min(), test_ts.max(), color="C1", alpha=0.3, label="Forecast horizon")

plt.legend()

plt.show()

We can now use train_data to train the predictor, and test_data to obtain an estimate of its performance on unseen data.

predictor = TimeSeriesPredictor(prediction_length=prediction_length, eval_metric="MASE").fit(train_data)

predictor.evaluate(test_data)

AutoGluon evaluates the performance of forecasting models by measuring how well their forecasts align with the actually observed time series.

For each time series in test_data, the predictor does the following:

Hold out the last

prediction_lengthvalues of the time series.Generate a forecast for the held out part of the time series, i.e., the forecast horizon.

Quantify how well the forecast matches the actually observed (held out) values of the time series using the

eval_metric.

Finally, the scores are averaged over all time series in the dataset.

The crucial detail here is that evaluate always computes the score on the last prediction_length time steps of each time series.

The beginning of each time series (except the last prediction_length time steps) is only used to initialize the models before forecasting.

Backtesting using multiple windows#

We can more accurately estimate the performance using backtest (i.e., evaluate performance on multiple forecast horizons generated from the same time series).

This can be done using a MultiWindowSplitter.

from autogluon.timeseries.splitter import MultiWindowSplitter

splitter = MultiWindowSplitter(num_windows=5)

train_data, test_data_multi_window = splitter.split(test_data, prediction_length)

predictor.evaluate(test_data_multi_window)

The new test set test_data_multi_window will now contain up to num_windows time series for each original time series in test_data.

The score will be computed on the last prediction_length time steps of each time series (marked in orange).

Multi-window backtesting typically results in more accurate estimation of the forecast quality on unseen data. However, this strategy decreases the amount of training data available for fitting models, so we recommend using single-window backtesting if the training time series are short.

How to choose and interpret the evaluation metric?#

Different evaluation metrics capture different properties of the forecast, and therefore depend on the application that the user has in mind. Here is a very rough guide outlining some scenarios when you can prefer different metrics:

mean_wQuantileLoss- if you care about the quantile forecasts (all other metrics ignore the quantile forecasts)MASEorsMAPE- if you care about an accurate forecast for each time series, regardless of its scaleMAE- if you care about accurately predicting time series with larger scale (e.g., accurately predicting demand for popular items)RMSE- similar toMAE, but penalizes large mispredictions more strongly

For more details about the available metrics, see the documentation for autogluon.timeseries.evaluator.TimeSeriesEvaluator or this article.

Note that AutoGluon always reports all metrics in a higher-is-better format.

For this purpose, some metrics are multiplied by -1.

For example, if we set eval_metric="MASE", the predictor will actually report -MASE (i.e., MASE score multiplied by -1). This means the test_score will be between 0 (best possible forecast) and \(-\infty\) (worst possible forecast).

How does AutoGluon perform validation?#

When we fit the predictor with predictor.fit(train_data=train_data), under the hood AutoGluon further splits the original dataset train_data into train and validation parts.

Performance of different models on the validation set is evaluated using the evaluate method, just like described above.

The model that achieves the best validation score will be used for prediction in the end.

By default, the internal validation set contains a single window containing the last prediction_length time steps of each time series. We can increase the number of validation windows using the num_val_windows argument.

predictor = TimeSeriesPredictor(...)

predictor.fit(train_data, num_val_windows=3)

This will reduce the likelihood of overfitting but will increase the training time approximately by a factor of num_val_windows.

Note that multiple validation windows can only be used if the time series in train_data have length of at least (num_val_windows + 1) * prediction_length.

Alternatively, a user can provide their own validation set to the fit method. In this case it’s important to remember that the validation score is computed on the last prediction_length time steps of each time series.

predictor.fit(train_data=train_data, tuning_data=my_validation_dataset)

Which forecasting models are available in AutoGluon?#

Forecasting models in AutoGluon can be divided into three broad categories: local, global, and ensemble models.

Local models are simple statistical models that are specifically designed to capture patterns such as trend or seasonality. Despite their simplicity, these models often produce reasonable forecasts and serve as a strong baseline. Some examples of available local models:

ETSARIMAThetaSeasonalNaive

If the dataset consists of multiple time series, we fit a separate local model to each time series — hence the name “local”. This means, if we want to make a forecast for a new time series that wasn’t part of the training set, all local models will be fit from scratch for the new time series.

Global models are machine learning algorithms that learn a single model from the entire training set consisting of multiple time series. Most global models in AutoGluon are provided by the GluonTS library. These are neural-network algorithms (implemented in PyTorch or MXNet), such as:

DeepARPatchTSTTemporalFusionTransformer

AutoGluon also offers two tabular global models RecursiveTabular and DirectTabular.

Under the hood, these models convert the forecasting task into a regression problem and use a TabularPredictor to fit regression algorithms like LightGBM.

Finally, an ensemble model works by combining predictions of all other models.

By default, TimeSeriesPredictor always fits a WeightedEnsemble on top of other models.

This can be disabled by setting enable_ensemble=False when calling the fit method.

For a list of tunable hyperparameters for each model, their default values, and other details see Forecasting Model Zoo.

What functionality does TimeSeriesPredictor offer?#

AutoGluon offers multiple ways to configure the behavior of a TimeSeriesPredictor that are suitable for both beginners and expert users.

Basic configuration with presets and time_limit#

We can fit TimeSeriesPredictor with different pre-defined configurations using the presets argument of the fit method.

predictor = TimeSeriesPredictor(...)

predictor.fit(train_data, presets="medium_quality")

Higher quality presets usually result in better forecasts but take longer to train. The following presets are available:

"fast_training": fit simple statistical models (ETS,Theta,Naive,SeasonalNaive) + fast tree-based modelRecursiveTabular. These models are fast to train but may not be very accurate."medium_quality": all models mentioned above + deep learning modelDeepAR. Default setting that produces good forecasts with reasonable training time."high_quality": all models mentioned above + automatically tuned statistical models (AutoETS,AutoARIMA) + tree-based modelDirectTabular+ deep learning modelsTemporalFusionTransformerandPatchTST. Much more accurate thanmedium_quality, but takes longer to train."best_quality": all models mentioned above + more tabular models + training multiple copies ofDeepAR. Usually better thanhigh_quality, but takes even longer to train.

Another way to control the training time is using the time_limit argument.

predictor.fit(

train_data,

time_limit=60 * 60, # total training time in seconds

)

If no time_limit is provided, the predictor will train until all models have been fit.

Manually configuring models#

Advanced users can override the presets and manually specify what models should be trained by the predictor using the hyperparameters argument.

predictor = TimeSeriesPredictor(...)

predictor.fit(

...

hyperparameters={

"DeepAR": {},

"ETS": [

{"seasonal": "add"},

{"seasonal": None},

],

}

)

The above example will train three models:

DeepARwith default hyperparametersETSwith additive seasonality (all other parameters set to their defaults)ETSwith seasonality disabled (all other parameters set to their defaults)

You can also exclude certain models from the presets using the excluded_model_type argument.

predictor.fit(

...

presets="high_quality",

excluded_model_types=["AutoETS", "AutoARIMA"],

)

For the full list of available models and the respective hyperparameters, see Forecasting Model Zoo.

Hyperparameter tuning#

Advanced users can define search spaces for model hyperparameters and let AutoGluon automatically determine the best configuration for the model.

from autogluon.common import space

predictor = TimeSeriesPredictor()

predictor.fit(

train_data,

hyperparameters={

"DeepAR": {

"hidden_size": space.Int(20, 100),

"dropout_rate": space.Categorical(0.1, 0.3),

},

},

hyperparameter_tune_kwargs="auto",

enable_ensemble=False,

)

This code will train multiple versions of the DeepAR model with 10 different hyperparameter configurations.

AutGluon will automatically select the best model configuration that achieves the highest validation score and use it for prediction.

AutoGluon uses different hyperparameter optimization (HPO) backends for different models:

Ray Tune for GluonTS models implemented in

MXNet(e.g.,DeepARMXNet,TemporalFusionTransformerMXNet)Custom backend implementing random search for all other models

We can change the number of random search runs by passing a dictionary as hyperparameter_tune_kwargs

predictor.fit(

...

hyperparameter_tune_kwargs={

"scheduler": "local",

"searcher": "random",

"num_trials": 20,

},

...

)

The hyperparameter_tune_kwargs dict must include the following keys:

"num_trials": int, number of configurations to train for each tuned model"searcher": one of"random"(random search),"bayes"(bayesian optimization for GluonTS MXNet models, random search for other models) and"auto"(same as"bayes")."scheduler": the only supported option is"local"(all models trained on the same machine)

Note: HPO significantly increases the training time for most models, but often provides only modest performance gains.